Revision And Preparations For Online College Monetary Policies Exam

Almost 1 million jobs were lost in manufacturing industry between 1979 and 1982. How did monetary policies contribute to this problem?

Explain the trade-off between wages and inflation using the Philips curve or the real-wage bargaining approach

Discuss the implications of traditional macroeconomic management of the economy

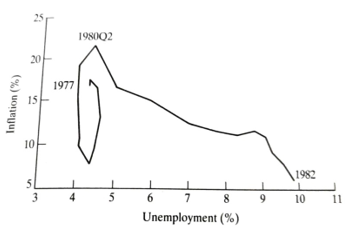

Figure 7.9 Retail price inflation and UK unemployment: 1977-82

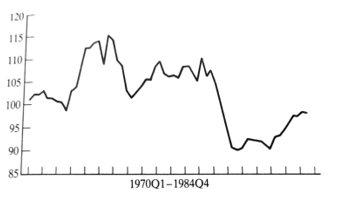

Figure 7.10 Index of industrial production (including energy and water supply), 1970-84, 1985=100

The rise in unemployment in the 1980s caused a resurgence of interest in incomes policies as a way of holding down wages and prices during a reflation of aggregate demand. Why do professional economists generally view income policies with skepticism?

Incomes policies have been tried from time to time in the United Kingdom, but they are generally viewed with skepticism by professional economists. The academic objection to incomes policy is usually based upon three propositions. The first is that independent wage-push is not the cause inflation and so an incomes policy must eventually be frustrated because does not tackle the root cause of the problem. This leads to the second point which is that while an incomes policy can have no long-run effect, it will work in holding down wages in some areas, and so there will be distortion introduced in the allocation of labor. The economy will thus be efficient. Finally, and perhaps strongest of all, is the point that it has proven extremely difficult to demonstrate that incomes policies have had any significant effect at all in the United Kingdom in the last twenty-five years Parkin, Sumner and Jones (1972), for example, in their survey of the evidence on this subject, conclude that:

On the basis of our present knowledge, it is possible to say that, with the exception of the immediate post-war experiment, incomes policy apparently has little effect either on the wage determination process or on the average rate of wage inflation. (p. 13)

The existing evidence indicates that incomes policies have had no identifiable effect on the price equation. (p. 25)

How then might an incomes policy work in the context of the model in Figure 7.7? It should be clear that the long-run position of the economy depends only upon the long-run budget constraint and upon the natural rate of unemployment or NAIRU. The long-run budget constraint depends entirely upon the policy-determined growth of monetary demand. So incomes policy could not influence the long-run inflation rate in this model. However, it could influence the short-run course of the economy if it succeeded in lowering inflationary expectations. In this case the short-run Phillips curve would shift down to the left. For a given short-run budget constraint inflation would be lower and employment would be higher than otherwise. If this could be achieved, then, even if the long-run inflation rate was unchanged, a higher average level of output and lower average unemployment could be attained. This would undoubtedly be preferable to the situation in which there was no incomes policy.

The problem with an incomes policy is that even if the initial effect is favorable, the belief that the policy is ending can have an equally adverse effect or even worse. The expectation of the collapse of an incomes policy would shift the short-run Phillips curve up to the right, thus making inflation and unemployment worse. Many economists believe that this is exactly what happens. A short-run benefit is fairly quickly offset by an equal deterioration. Henry and Ormerod (1978), for example, conclude that

Whilst some incomes policies have reduced the rate of wage inflation during the period in which they operated, this reduction has only been temporary. Wage increases in the period immediately following the ending of the policies were higher than they would otherwise have been, and these increases match losses incurred during the operation of the incomes policy. (p. 39) Thus while it is logically possible that incomes policies could improve the dynamic path towards any long-run inflation rate, there is no evidence that they have done so in the recent past. Any short-run benefit in terms of higher employment and lower inflation is subsequently offset by higher inflation and lower employment as the policy breaks down. There are two possible stories about this breakdown. The first is the catching up of expectations that have been mentioned above. The second gives a critical role to the public sector. It is argued that incomes policies have their greatest impact on public sector wages since the government is in effect itself the employer, whereas private sector employers can get around the policy if market conditions demand. As time passes the public sector employees notice that their wages are falling behind comparable private sector groups and demand 'pay comparability'. This leads to substantial public sector 'catch up' awards which effectively herald the end of the incomes policy. In 1979 the Labor Government even went so far as to set up a Public Sector Comparability Commission to deal with the multiplicity of public sector groups who felt that they had suffered under successive phases of incomes policies.

This points to the existence of two separate problems in this area. The first is how to make incomes policies more widely effective and other than in the short run. The answer to this is that it is probably not worth trying. Since the administrative and distortionary costs would seem to be prohibitive in peacetime. The second problem is how to determine public sector wages. The larger is the public sector share of employment the more inappropriate it becomes to set public sector wages by comparison with the private sector. In the end there could be just one person left in the private sector whose wages determine those for the rest of the economy! A more coherent public wages policy is required which is made consistent with other aspects of policy such as employment and public expenditure targets and bears a sensible relationship to the underlying growth pattern of the real economy. Neither the adoption nor the abandonment of incomes policies obviates the need for a sensible policy towards public sector pay.

In one sense, the failure of past incomes policies is that they impose a regulatory solution to a market failure. The market failure in this case is essentially one of coordination. In terms of the Phillips curve, all parties in the economy would like to be at the natural rate with zero inflation. The aim of an incomes policy is to move us straight to this 'bliss' point. On the of it, an external, legislative policy can be seen as a perfect example of a pre-commitment, which, as we saw in Chapter 4, is one means of achieving otherwise unattainable positions. However, regulatory solutions to macro-economic problems carry with them the baggage of microeconomics inefficiencies, and this dilutes the credibility of the commitment. What would be preferred, therefore, is some solution that would make the best interests of each party-crudely, firms and unions to voluntarily choose the optimum level of inflation and employment. Two proposals have been made along these lines: tax-based incomes policies, and a reform of the Tax-based incomes policies were introduced into the UK policy de collective bargaining system by Jackman and Layard (1982, 1986, 1990). The basic idea is to tax excessive wage increases. This increases the incentive for firms to resist rises, and makes higher wages costlier for unions (in terms of lost jobs from higher wage costs). So, wage (and subsequently price) inflation is reduced. B proponents of the scheme go further and argue that the NAIRU itself will be reduced. In terms of the bargaining approach to the Phillips curve discussed above, it reduces the target real wage as the marginal trade-off between wages and unemployment is worsened. In effect, the NAIRU is reduced in terms of Figure 7.7, the long-run Phillips curve shifts to the left. It may seem paradoxical that a rise in labor taxes should lead to a fall in unemployment. However, the fiscal impact is designed to be neutral - a blanket subsidy is given to all firms financed by the wage inflation tax while the incentive effects remain in place. Thus, the tax-based incomes policy substitutes private incentives for the regulatory enforcement problem.

The main problem with the policy is that it fails to distinguish productivity-based increases in wages and inflationary ones. The former is efficient, in the sense that they reward higher productivity; indeed, efficient allocation of resources requires price signals of this kind. It is hard to assess how large a distortion this will create. In some sectors at some times, it could be very large. It would have the effect of precisely targeting fast-growing areas with higher taxes; for example, computer software design would have been singled out in the late 1980s. This is a peculiar industrial policy. It is also unclear how robust the theoretical results are when the labor market model is extended to richer characterizations than the right-to-manage model. For these reasons, the case for a permanent policy of this type may be weaker than its proponents suggest although the distortions it engenders are likely to be less than those observed under the conventional type of policy.

Do you agree there’s a serious problem with the wage rigidity in the UK labor market?

Reform of the wage bargaining system has also been advocated in the United Kingdom. Most observers agree that there is a serious problem of wage rigidity in the UK labor market. Wages adjust only slowly to demand and supply shocks, exacerbating the resulting problems of slow growth and high unemployment. Countries with highly decentralized bargaining systems and low union power seem to be more responsive than the United Kingdom. Japan is the prime example of this, although there are other factors at work there. There is clear evidence that wages respond more to aggregate shocks, and employment less, in Japan. So the anti-union policies pursued in the 1980s in the United Kingdom can be seen as anti-inflationary but their effect seems to have been remarkably small. After three years of continuous falls in non-oil GDP, UK real wages were still rising at about 4 per cent per annum in April 1993; this does not look like strong evidence for a weak labor force. Recall the discussion earlier in the chapter relating to insiders and outsiders.

Nevertheless, there do exist alternative ways to organize wage-bargaining that seem to offer equivalent benefits to full competition. In Scandinavia and Austria powerful unions bargain centrally with national employers’ organizations in a coordinated bargaining process. To some extent, this happens in the Japanese Shunto, or 'spring offensive' on wages. From an economic point of view, the advantage is that an external cost (inflation) is internalized. The problem with decentralized uncoordinated bargaining is that, in effect, competitive unions and firms bid wages up against each other. The aggregate effect of a given wage increase over the underlying increase in productivity is (roughly) to 'simply increase prices by that amount. So collectively it makes sense to restrict wage increases. For an individual union the effect of its own wage increase on the aggregate price level is vanishingly small, so there is no incentive to take account of the aggregate effect. As all unions are in this position, and similarly all firms willing to accede to wage demands without taking account of the aggregate effect, the result is high inflation. By contrast, if unions and firms are able to act collectively, then a mutually beneficial outcome is attainable, with (say) the same real wage outcome, but at lower inflation. If such institutions had existed in the United Kingdom, then perhaps the unemployment explosions of the early and late 1980s could have been avoided. What is needed to make this kind of outcome work is unclear. Several elements may be required. First, national union and employers' organizations needed. Furthermore, these organizations must be able to enforce agreements. As usual in game-theoretic problems like this, there is a free-rider problem. If national negotiators achieve low inflation, then any local bargain over the national norm constitutes a real increase. So there is a strong incentive for individual unions to bid for higher wages. In the absence of a legislative framework or tough penalties on miscreants, a degree of social cohesion is required to make the process work. This does seem to exist in some of the Social Democratic North European countries and in Japan; it is less clear if it will work in the Anglo-Saxon countries," and especially in Britain.

Second, a national forum for debate has to exist. This (probably) involves explicit tripartite talks between government, unions and employers. It also requires a national debate to take place in order to help establish a consensus view of the state of the economy, informed by recognized and independent bodies. In the United Kingdom such independent bodies do exist, in the form of the independent forecasting teams, notably the National Institute for Social and Economic Research and Centre for Economic Forecasting at the London Business School, and the Institute for Fiscal Studies. The City also has a role to play here. When absent is a forum within which the three concerned parties can meet negotiate. Indeed, the closest thing to such an institution, the Nation Economic Development Office (NEDO), has recently been dismantled the government. A third precondition is that the wage bargaining timeshi probably needs to be compressed into a short period, essentially to coordination and to avoid news being used as a device for justify divergence from the norm. If these preconditions were met, there is a strong chance that inflation would be lower and wages more responsive to shocks. However, it is not at all clear that the social structure of the United Kingdom is consistent with this kind of institution.

It's impossible to understand Britain’s economy and changes in unemployment without considering factors that affect the equilibrium rate of unemployment. TRUE or FALSE

Britain is a small economy in a big world. Some of its economic history explained by world developments alone. However, the inflation of the mid-1970s and the unemployment of the early 1980s were both worse than could be blamed upon developments in the world economy. The former is largely explained by the excessive fiscal and monetary expansion of the 1971-73 period. The latter results from an over-appreciation of sterling caused by a combination of North Sea oil and tight monetary policies. There is also the extreme persistence of unemployment and the rise in real wages to explain, the causes of which are still uncertain, although we have offered possible explanations. As we will see in Chapter 8 on financial deregulation, the most recent rise in unemployment (between 1990 and 1993) was largely due to the slump in consumers' expenditure caused by the collapse of the mid-1980s credit boom, itself caused at least in part by a fundamental deregulation of the UK financial system. Thus, although we cannot hope to understand changes in unemployment by ignoring factors that affect the equilibrium rate of unemployment, the 'natural rate' framework for the analysis of unemployment gives only a part of the answer.