4 Common Questions to Help You Revise and Prepare for Your Online Tax and Spending Exams

Discuss the concept of crowding out

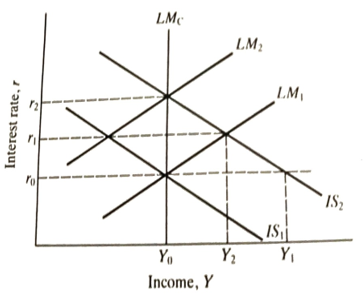

With the help of a graph, explain how crowding out affects the classical IS-LM model. Show the shifts in the LM and IS curves as government expenditure and interest rates change.

Fig 10.1 Crowding out in the Classical IS-LM model.

Crowding out of private investment, say, on LM1 at an interest rate of r1 However, the rise in income from Y0 to Y1 could represent a multiplier in excess of unity.

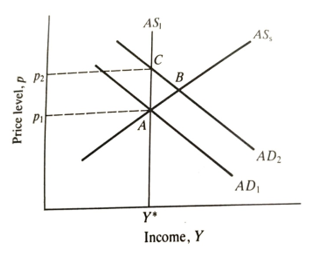

Illustrate how an increase in government expenditure moves the economy in the classical AD-AS model

It should be clear that if we add a supply side to the model, crowding out will be even more likely to occur. This is pictured in Figure 10.2. The short-run aggregate supply curve AS, is upward sloping because labour supply depends upon expected prices, whereas demand for labour depends upon actual prices. There is a rise in output in the short run because expectations lag behind actuality and so there is a temporary fall in the real wage. More labour is employed and more output produced.

An initial increase in government expenditure would move the economy.

Figure 10.2 Crowding out in the Classical AD-AS model.

from A to B (ignoring the government budget constraint). However, over time price expectations will catch up with reality and, as they does, the short-run aggregate supply curve will shift up to the left. Eventually the economy will settle again at C where output is on the long-run aggregate supply curve. The increase in government expenditure will have crowded out private expenditures of an equal amount. It will be largely private investment that is crowded out, since the fall in the real money stock will raise interest rates Thus the story we are left with from this model is that crowding out is quite likely in the long run but there may be a short period during which government expenditure leads to income increases through the multiplier process. Only if the economy could be shown to start off well to the left of the 4S, curve, and not to be there because of an inflation cycle, could we argue that there was a chance that there would be no long-run crowding out.

An additional factor which could increase the likelihood of short-run crowding out would be if price expectations are formed 'rationally', in the sense defined in Chapter 4. It has implicitly been assumed above that price expectations are formed adaptively, as a revision from the prediction error made last time. If, however, all actors understand the model and realize that the expansion of government expenditure is going to raise prices, it could be that there will be no short-run output gain at all. Rather, the AS, curve will shift up rapidly and the economy will go straight from A to C. This is the source of the argument that only unanticipated policy changes will have any real effects.

The remaining question concerns the position of the long-run supply curve. It has been argued that this will be positioned at the level of output corresponding to the NAIRU-the natural rate of output. This is basically determined from year to year by the underlying growth trend of the economy. It would seem from the above analysis that the only chance of long-run crowding out not occurring is if rises in government expenditure can increase the underlying growth potential of the economy. This is certainly possible; we examine this question in more detail at the end of this chapter. Nevertheless, the most vociferous commentators on this issue believe that exactly the opposite will occur. Brunner and Meltzer (1976, p. 769), for example, argue that:

Reduction in the output of the private sector could, in principle, be offset by the increased output of the public sector, it does not happen. Instead, there are loans or subsidies to enterprises that earn no profit or suffer large losses. Private saving is directed, in this case, toward enterprises that often do not earn rates of return equal to the interest on the bonds issued to finance the government budget deficit. Or, investment is used to increase 'prestige' as in the case of Concorde, national airlines, steamship lines and other enterprises that operate at negative rates of return. These enterprises direct material, skilled labour, and capital toward less productive uses than the private output that is crowded out. The list of such enterprises can be Absorption of labour by the government does not substitute public out expanded by every knowledgeable reader.

Absorption of labour by the government does not substitute public output for private output of equivalent value. Much public employment has the opposite effect. Complex rules and regulations absorb the time of civil servants and create demands in the private sector for lawyers, accountants, negotiators and clerks to keep abreast of the rules, to fill out the forms and hopefully to obtain more favourable interpretations than competitors have obtained.

Explain ways in which we can test for the presence of crowding out

One way of testing for the presence of crowding out is to use estimated econometric forecasting models to simulate the effects of various policy changes. The Macroeconomic Modeling Bureau based at Warwick University regularly undertakes comparative simulations of the major UK models. Church and Whitley (1991) present the results of simulations on the Treasury and Bank of England (and other) models (as of June 1991). As a cautionary preamble, it is worth recalling the criticisms of this procedure made by Robert Lucas (see Chapter 4 in this book). Such exercises require the structural model of the economy to be policy invariant. There is no reason to believe that this is so. As a result, the safest conclusion is that these simulations tell us a lot about the properties of the model in question but, perhaps, not very much about the properties of the economy itself.

Table 10.1 reports the effects produced in the Treasury and Bank of England models of a rise in government spending under two different assumptions. The first simulation is for a rise of government consumption of £2bn, holding interest rates fixed, while the second fixes the exchange rate. The simulations allow the full range of supply and demand effects to work through. The long-run multiplier implied by the models for both taxes and government spending is about one, although the effects on other variables like inflation and the balance of payments differ between the two cases; for example, a cut in income tax tends to reduce pressure on wages so inflation is lower than when government spending rises. The effect on the balance of trade is the reverse, but as the table shows, the results are very sensitive to the assumption about the exchange rate. If the exchange rate is fixed, then the consequences of a rise in government spending are quite different; output falls, and the multiplier is negative. If nothing else, this

Table 10.1 Percentage effect on real GDP of a £2 billion rise in government spending (1990 prices) and equivalent fall in income tax.

Year |

Bank |

HMT |

||||

|---|---|---|---|---|---|---|

1 |

3 |

5 |

1 |

3 |

5 |

|

G (i) |

0.40 |

0.53 |

0.56 |

0.43 |

0.50 |

0.46 |

G (ii) |

0.36 |

-0.20 |

-1.10 |

0.39 |

0.15 |

-0.36 |

T (i) |

0.13 |

0.40 |

0.59 |

0.11 |

0.34 |

0.52 |

Notes: (i) fixed interest rate; (1) fixed exchange rate.

example serves as a salutary lesson about the relationship between simple economic theory and actual economies. In theory, a boost to government spending raises interest rates which leads to upward pressure on the pound; the government is forced to respond by expanding the money supply and reducing interest rates, thus expanding the economy. In the 'real' model, the worsening current account leads to a potential depreciation, forcing higher interest rates in defense of the exchange rate, reducing aggregate demand.