Well-Answered Questions to Guide You When Preparing For Your Management Exam

Why are company objectives in management very important and how can they be achieved?

What are the main components of management objectives?

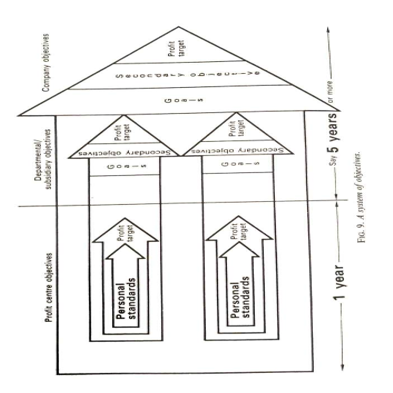

Fig 9 A Systems of Objectives

Question

What role do managers play in achieving the company’s profit targets?

Answer

The first component of the family of objectives is the profit target, or objective. Profit must be the prime motivation for all companies, except those who are formed as a charity or similar purpose. Many managers will argue that their objective is to maximize profits. The only problems with this definition are that nobody knows what it really means, and there is no method of telling when it has been achieved. In most cases it also happens to be untrue: no company is prepared to do anything for profit for example, some companies may hold that profits connected with the betting industry are immoral, and few would now insist on working their employees into a state of complete physical and mental exhaustion. In dealings with their customers, most companies are likely to argue that they must act in such a way that the customer is likely to repeat purchases in the future, as they are not looking for high profits that end with the first order, but a source of profits stretching out to some future time horizon. So the definition that "our objective is to maximize profits over the long term" is coined. Unfortunately, this too is meaningless.

Return on investment itself can be a mixture of numerous items. Assets may be in the books at various values: at original purchase price, at a revaluation, or depreciated. What the accountants call goodwill when the acquisition of a business costs more than the value of its assets may or may not have been written off. I do not believe that this renders the concept of return on investment meaningless, provided the company sets itself a series of house rules to work to. This means that the capital employed figures may differ from those in the books: for instance, I think there is a good argument for not writing off goodwill in the management control figures. Having set its rules, the company has one of the parameters of its profit target.

In fact this parameter should be defined and expressed in two ways. From the management viewpoint, return on capital employed provides criteria of effectiveness. The shareholder is more interested in a return on equity capital, and this must also be taken into account. Return on shareholders' capital could drop because of a change in gearing, even though profits were rising: this would affect the dividend earnings per share, which in turn could cause changes in stock market prices.

The second element of the target is a rate of profit growth, on a defined base. So the target might be expressed in terms like these:

The target for the next 5 years is an annual growth of after tax profits of 5%, provided that a minimum return on capital employed of 10% is maintained.

This shows the sort of target that can be established, but we still have to think about the things a company might consider to arrive at these figures.

Whatever target is set has to satisfy the people who own the business. So one guide-line that should be taken is the return and growth rate which the company has achieved in previous years. This provides a base line. Now if this is below the performance of other similar companies-and we must accept that it is difficult to find exactly comparable data, so any results will be approximate-the chief executive may feel that he is setting his sights too low, and may upgrade his target. The chief executive may decide that even this improved target is not good enough, and that he must increase above this. Whatever target he sets, he will want to review it in the light of the corporate appraisal, to make sure that it is neither below nor above the capacity of the firm. One thing he can never do with impunity is to set targets which reflect a worsening of performance. Shareholders do not like to take cuts in their dividend!

In recent years the use of a profit objective expressed in growth in earnings per share has found considerable favour. This has the advantage of relating profits to the shareholders' stake in the company. It could lead to financial policies based on loan finance rather than risking reducing the earnings per share by increasing the number of shares. Overall it is good measure.

The company profit target must eventually be broken down into targets for each division (or subsidiary) of the company, and for each profit centre. The chief executive should not make the mistake of setting the same growth and return on capital employed targets for each division. One area of the company may yield a 30% R.O.I., another may struggle to make 10%. One may have fast growth profits: another may be in a mature market. These varying returns may reflect the differing degrees of risk attached to each business area. It may be very wise to have low yielding sector of the company, which can be guaranteed to turn in a certain level of profits, and seeking to achieve the total company target through a balance with high yield, but higher risk, projects. But this is moving into the realms of strategy.

Profit centre targets are probably best set by the division controlling them. It may be that only yearly targets are required at this level. It is also possible that a further modification of the R.O.I. concept is desirable. For example, a company might operate three shops of identical size, yielding about the same profit. If one was purchased in 1930, another in 1968, and the third is rented, there will be a completely different capital employed structure. It would be necessary for the manager of the 1968 shop to be four or five times as efficient as the other managers, in order to obtain the same R.O.I. What may be a better motivating target is one which is adjusted for these differences perhaps all buildings valued on a 1968 basis (including the rented one), and earning adjusted by a rent/depreciation factor. The reasoning is not, of course, to make the task of the manager of the 1968 shop easier-he must still yield an R.O.I. acceptable to the company! It is to upgrade the targets of the other managers in a fair way. Inflation accounting would go a long way in helping to set these targets.

Question

Besides profits what other objectives should every company strive to achieve?

Answer

The next group of objectives (for want of a better description) may be termed secondary objectives. This is not to suggest that they are inferior or in any way less important than the profit target. Both concepts are required if the company's system of objectives is to be a truly motivating force. At the total company level the secondary objective is a description of the nature of the company's business (the term "mission" is used in some books). First the question "What is my business?" should be asked. (This is established in the corporate appraisal, although a preliminary definition can be made beforehand.) This is not the objective, which is revealed by the answer to the next important question to be asked "What should my business be? This particular concept is, therefore, the definition in as concise a way as possible of the type of company the chief executive intends to have at some future date.

Those who criticize this approach argue that a definition such as this really falls into the realm of corporate strategy. There is truth in this, but there is a counter argument. Firstly, it does not matter anyway if the concept does trespass a little, because none of the steps in the planning process are completely isolated from the others, and indeed, each overlaps every other one to a certain extent.

The second argument is even more powerful. There is a concept of what a company should be in the minds of every chief executive, regardless of his strategy. For example, there is a very real difference in corporate purpose between a conglomerate company which is willing to make an investment in any field, provided it is profitable, and a company operating in one or two industries which would never consider moving into a new area. It may be that the day will come when the second company will have to change its objectives, but this in itself is not wrong. There is a similarity with the. Objectives of a person as he matures. As he gains in experience and education, as he obtains family and other responsibilities, so his concept of his ultimate aims changes. So it is with a company. There is no reason to expect any targets set today to be the right ones for the next hundred years and this applies to the profit targets as well.

Of course it is important for an objective to be stated in terms that lead the company in the right direction. Too narrow a definition can be stilting-the wrong map grid reference mentioned earlier. A company supplying coal might put itself in a strait-jacket if it saw its business as simply the "supply of coal to households". A broader definition "The corporate objective is the marketing and distribution of home fuel requirements" might help the chief executive to see opportunities in the sale of paraffin or domestic fuel oil of marketing his fuel through untraditional channels, such as the pre-packed solid fuel now passing through greengrocers.

This looks very obvious, and the immediate reaction might be that the coal merchant might see this as his business without being so specific. There are many examples where management within narrow limits of vision has lost many opportunities to a company. For many years the railway undertakings saw themselves simply as being enterprises engaged in the running of trains, rather than in the physical distribution business. Some shipping companies might now consider that they are as much in the hotel and entertainment business (luxury cruises, for example), as in the activity of transporting goods and passengers from A to B. Perhaps some grocery wholesalers who once had a conception of themselves as warehouse operators, transporters, and sellers to retailers, now consider their main task is to help retailers who deal with them to make a profit. This must be one driving force in the voluntary chain movement.

Other types of objective should also be set, to cover each of the key sectors of total company performance. A small family of secondary objectives will be formed. Examples of other areas where further definition may be required are in relations with company personnel, with government, perhaps even to such items as the type of corporate image the chief executive intends his company to have.

These statements should be as specific as possible (quantification is a good rule to follow, and even the objective for the corporate image can be quantified), and above all they must be true statements of intent. If the company does not consider any particular aspect important, it should not frame an objective to cover it. The example above of relations with government is a case in point. Some companies hold to the principle of being "good citizens" of every country in which they operate. This policy can have a far-reaching effect on their operations. That great American giant Union Carbide takes relations with governments so seriously that it has set up a special department to foster contact and co-operation. Other companies have no such policy, and may feel that they do not wish to obtain any particular relationship with government-only to stay within the letter of the law.

The modern tendency is for companies to acknowledge that they have a plurality of "stakeholders", employees, shareholders, the community, customers and suppliers all of whom have expectations from the company. Objectives need to be defined in each area. The shareholders are no longer the only important influence on the aims and behavior of the firm. The concept of secondary objectives goes further.

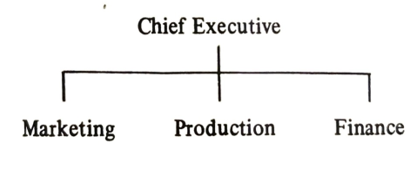

FIG. 10. Company Organized on Simple Lines

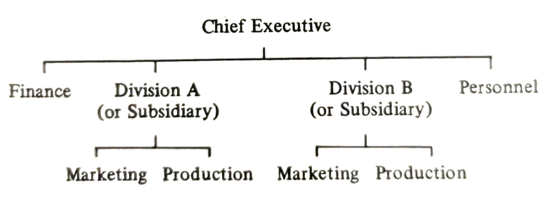

A more complex company, as in Fig. 11, could well have one level of objectives for each division or subsidiary which are similar in scope to the overall corporate objectives, and to which the same principles apply, and a further level, similar to those of the "simple" company, for each function within the divisions.

Many of these objectives do fall right under the heading of strategy, since they can only be determined in areas of the strategic decisions. Marketing Production Marketing Production

FIG. 11. Company Organized on More Complex Lines.